Overview

Making sense of the fast-moving and complex policy landscape can be daunting, particularly for SMEs and new entrants to the aerospace sector. An awareness of the policy landscape, including ongoing initiatives, emerging support, and the long-term aspirations for the sector, can help organisations understand how their activities can contribute to the industry’s transition towards Net Zero, and the business opportunities that could be generated along the way.

Sustainability is of vital importance as it supports the competitiveness of the UK aerospace industry. The global aerospace market value is £4.3 trillion up to 2050, providing a significant opportunity for UK businesses to expand market share and benefit from the sector’s transition to net zero through the introduction of sustainable aircraft technologies.

While not exhaustive, this overview will provide a glance at the key pieces of legislation, focusing on the UK, but also touching on that of the EU, US and the wider international context, to explain the converging and diverging policy landscape. Links have been provided in the headings for each policy measure should you wish to find out more.

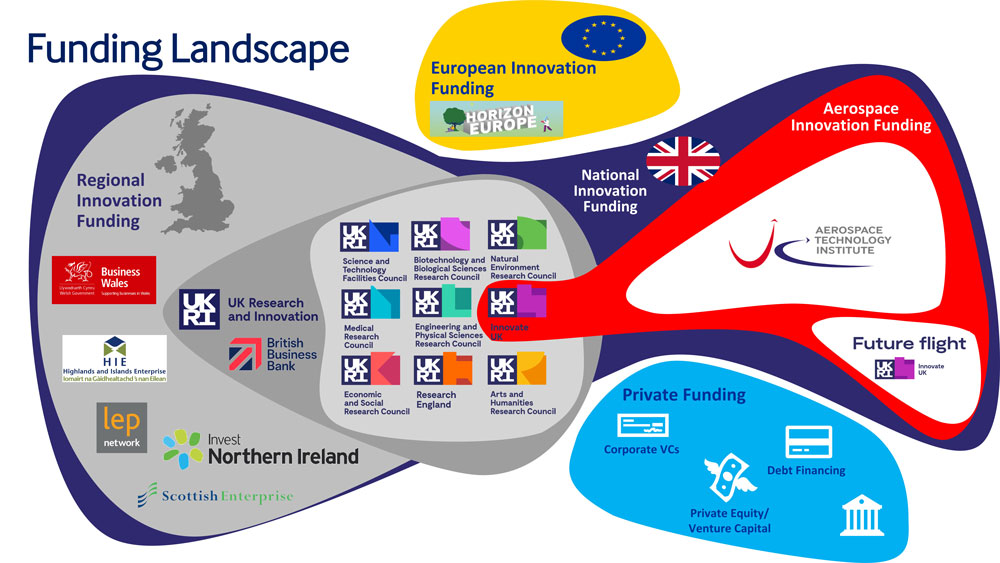

The funding landscape is a key element of policy which can provide R&D support to the aerospace sector to help achieve decarbonisation. An overview of this is provided separately at this link. Also published on the Hub is an introduction to the UK Civil Aviation Authority (CAA), covering their regulatory role in aviation.

This resource was updated in November 2025.

Please note the ATI is not responsible for the content provided in the links to third party websites included in this resource.

UK policy

The UK’s air transport sector is making progress towards Net Zero through collaborative working and partnerships between government and industry. A combination of voluntary measures and regulatory developments, guided by scientific understanding and industry advice is helping to build a strong landscape in which investment and technological development can thrive.

The government’s overarching sustainability target is a 100% reduction in greenhouse gas emissions by 2050, referred to as the Net Zero target. This was made legally binding by the Climate Change Act 2008 (2050 Target Amendment) Order 2019. Soon after establishing this target, interim targets were also set to reduce carbon emissions by 68% by 2030 compared to 1990 levels and 81% by 2035. These provide the overall objective from which government support and frameworks for a sustainable aerospace and aviation industry evolved. The policy measures outlined below detail the government’s actions to progress towards achieving these targets.

The Jet Zero Strategy is the UK government’s plan for achieving Net Zero aviation by 2050. The strategy includes a 5-year delivery plan to support decarbonisation through six policy measures:

Several specific policy measures and aspirations are proposed in the strategy. These include (but are not limited to):

- Achieving 2040 zero emissions airports

- Achieving 2040 domestic Net Zero aviation

- Sustainable Aviation Fuels (SAF)

- Having at least five commercial scale SAF plants under construction in the UK by 2025. The Advanced Fuels Fund was launched to support this aim, competitively allocating £165 million in grant funding to support UK advanced fuels projects.

- A SAF Clearing House has been established in the UK and launched in summer 2023 to develop, test, validate and certify zero-carbon and sustainable aviation fuels.

- Achieving 10% SAF in the fuel supply by 2030.The strategy is due to be reviewed every five years, starting in 2027. In many areas (including achieving zero emissions flight and addressing non-CO2 emissions), further policy support is likely to be required, the details of which are anticipated to emerge as the science and technological opportunities are further developed. While progress has been made, the establishment of a domestic SAF industry has been slow, and further policy support may be required to develop this at pace to meet demand, be globally competitive and progress energy security in the UK.

UK Emissions Trading Scheme

The UK Emissions Trading Scheme (ETS) operates as a market-based approach and was adopted to replace the EU ETS after the departure from the EU. The UK ETS allows annual emissions across all sectors included in the scheme to be capped. Companies are required to purchase and retire carbon allowances (certificates) equal to their emissions, and the cap is reduced over time. This mechanism establishes a price for carbon emissions and allows for the trading of certificates, thereby incentivising companies to reduce emissions to cut costs.

The UK ETS specifically targets hard-to-abate and energy-intensive industries such as power generation and aviation. The UK Emissions Trading Scheme (UK ETS) issues free carbon allowances to some sectors to ensure international competitiveness is maintained and to limit carbon leakage (see CBAM section below). The aviation sector will lose all free allowances by 2026. Consequently, innovations in aerospace technologies that diminish the carbon footprint of air travel appeal to customers due to potential fuel savings and alleviating the financial strain imposed by the ETS.

In 2023 the UK ETS Authority committed to integrating engineered greenhouse gas removals into the UK ETS to support the development and scale-up of the technology. A consultation was conducted in 2024 to determine how this could be achieved, and the technical details and pathway for integration are yet to be confirmed.

Sustainable Aviation Fuels (SAF) Mandate

The SAF mandate came into effect in 2025. It establishes progressive targets for UK SAF use, starting at 2% (approximately 230,000 tonnes compared to a baseline of 64,000 tonnes in 2023) and increasing to 10% by 2030 and 22% by 2040. Other key policy elements include a limit on fuels made from HEFA (refined waste materials, cooking oils, and fats), a separate Power-to-Liquid (PtL) mandate and a buy-out price option for cases where fuel suppliers cannot secure the necessary volumes of SAF. SAF is expected to meet technical and sustainability criteria, such as being sourced from non-recyclable

To address the limitations associated with HEFA supply, the mandate proposes investments in innovation and diversification to support the development of more advanced SAF technologies, such as PtL with more scalable feedstock and a potential for greater emission reductions. As part of the mandate, 0.2% of the total jet fuel supplied in the UK will need to be PtL SAF from 2028, with targets increasing to 0.5% by 2030 and 3.5% by 2040. A cap on HEFA-produced SAF will be introduced, starting at 92% in 2027 and decreasing to 71% by 2030 and 35% by 2040.

The UK SAF Mandate functions as a tradeable certificate scheme, rewarding suppliers based on GHG emissions reductions. These certificates can be used to fulfil obligations or be traded. To incentivise supply and protect consumers, the buy-out options allow fuel suppliers to pay a fee (price per litre) with prices set at £4.70 per litre for HEFA-produced SAF covering the main SAF obligation and £5.00 per litre for PtL SAF, to be introduced in 2028.

UK Carbon Border Adjustment Mechanism (CBAM)

In March 2023, the UK government initiated consultations on CBAM to complement existing measures like the UK Emissions Trading Scheme (ETS).

In a bid to address carbon leakage risks, the CBAM targets imports of precursor commodities such as hydrogen, cement, ceramics, aluminium, iron, and steel. The proposed charges will account for the difference in carbon emissions during production and the discrepancy between carbon pricing in the country of origin and the UK. This adjustment may impact industries such as aircraft and engine manufacturing by adding carbon costs to raw materials like aluminium and steel. The ongoing consultation is set to conclude in June 2024, with the implementation of the CBAM planned for 2027.

Invest 2035: The UK’s modern industrial strategy

Invest 2035 is the UK’s 10-year plan to achieve strong industrial growth by providing certainty, stability and support to high-growth sectors and encouraging investment. The strategy identifies aerospace as an internationally competitive and growth-driving sector, and outlines how targeted support will boost productivity, innovation and global competitiveness. The net zero transition is recognised as a key opportunity, and support for R&D, skills and talent development, infrastructure and streamlined regulatory frameworks are all identified as ways to maximise this opportunity.

The strategy includes a 10-year funding commitment to the ATI Programme worth up to £2.3bn to 2035. This provides long-term certainty and stability for the sector, promoting investor confidence and enhancing the UK’s role in developing ultra-efficient and zero-carbon emission aircraft.

Advanced Manufacturing Sector Plan

In ‘Invest 2035: The UK’s modern industrial strategy’, 8 sectors were identified that have the greatest growth potential over the next decade and a critical role to play in supporting economic growth, resilience, and net zero. Bespoke sector plans have been developed for each, and the Advanced Manufacturing (AM) sector plan outlines the government support available to maximise growth, investment, jobs and stability in the sector and realise the economic opportunities of AM clusters. AM is particularly relevant to advancing sustainability in the aerospace industry due to its role in developing more efficient components and supporting the delivery of ultra-efficient and zero-carbon aircraft technologies.

UK Carbon Border Adjustment Mechanism (CBAM)

In a bid to address carbon leakage and ensure a level playing field for domestic industries, the CBAM requires importers of precursor commodities such as hydrogen, cement, ceramics, aluminium, iron, and steel to report and pay for embedded carbon emissions. The charges will account for the difference in carbon emissions during production and the discrepancy between carbon pricing in the country of origin and the UK. This adjustment may impact industries such as aircraft and engine manufacturing by adding carbon costs to raw materials like aluminium and steel. Free allocations in the UK ETS will start to reduce in affected sectors as the CBAM mechanism is gradually brought in and the potential for carbon leakage is addressed.

Following a consultation in 2023, the UK’s CBAM is set to begin in 2027.

UK Hydrogen Strategy

This strategy sets out how the UK will drive progress to deliver the ambition to produce 10GW of low-carbon hydrogen by 2030, with a twin-track approach of 4GW from carbon capture and storage (CCS)-enabled hydrogen and 6GW from electrolytic (green) hydrogen. It also positions hydrogen as one of a handful of new, low carbon solutions that will be critical to help meet the UK’s sixth carbon budget and Net Zero commitments. While not specific to aviation, the strategy outlines the steps that the government is taking to increase the commercial availability of hydrogen fuel. This includes support to ramp up production and development of the network and storage infrastructure, developing a market framework and supportive regulation, attracting investment and realising the full economic benefits for the UK. Economic benefits will be maximised by creating jobs, upskilling the workforce, increasing research and innovation, and taking full advantage of the export opportunities.

The strategy also recognises the potential of hydrogen in aviation’s transition to Net Zero, both as a potential fuel and as a requirement for synthetic SAF production. The UK aerospace sector is advancing hydrogen aircraft technologies at pace. The production of the hydrogen fuel, and liquefaction for use in larger aircraft will generate high demand for energy and will require significant increases in clean electricity generation. The Future of Hydrogen – Analysis – IEA

EU policy

The EU is currently on track to meet its 2030 target of a 55% reduction in emissions, and the European Commission has proposed an amendment to the EU Climate Law, setting a new 2040 target of a 90% reduction in net greenhouse gas emissions compared to 1990 levels. The EU remains committed to achieving net zero by 2050. This commitment is supported by member states and is also reflected in commitments and actions across the aerospace industry. Policy support mechanisms and regulatory drivers are in place to accelerate this transition and continue to evolve. Despite the make-up of the EU slowing the development and emergence of policy, the EU is still often considered a global leader in the Net Zero transition.

European Green Deal

This deal, approved in 2020, is a set of policy initiatives by the European Commission with the overarching aim of achieving the EU’s climate targets (detailed above). It sets the strategy for Net Zero while supporting growth and social sustainability across the EU. It also sets the policies for reducing net greenhouse gas emissions, described as the Fit for 55 packages of legislation (part of which is ReFuelEU Aviation detailed below).

EU Emissions Trading Scheme

The EU ETS is a key tool through which carbon emissions from hard-to-abate industries are capped and reduced over time. The EU ETS operates in the same manner as the UK ETS, and it is currently the world’s largest carbon market. Free allowances for airlines have been gradually phased out in recent years, and from 2026 these will no longer be available. From 2025 a monitoring, reporting and verification (MRV) system for non-CO2 effects also came into effect, with a report anticipated at the end of 2027 outlining legislative proposals for addressing these emissions. The limitations detailed above for the UK ETS also apply in the EU.

ReFuelEU Aviation

Commencing in 2025, ReFuelEU Aviation introduced a 2% SAF blending mandate for fuel suppliers, increasing every five years up to 70% by 2050. It also requires airlines departing from airports within the EU to refuel only with that necessary to complete the flight to avoid emissions associated with carrying enough fuel for the return flight, known as tankering. Under the legislation, EU airports must provide the infrastructure necessary to receive, store and refuel aircraft with the mandated SAF levels.

Renewable Energy Directive

This directive is the legal framework for the development of renewable energy across all sectors of the EU economy. It encourages cooperation between EU countries towards this goal and sets a legally binding target of at least 42.5% energy to be from renewable sources by 2030, with the aspiration to achieve 45%.

Net Zero Industry Act

This act aims to scale up the manufacturing of clean technologies in the EU. It aims to attract investment, create better market conditions and access, and simplify the regulatory framework for the manufacturing of these technologies. It hopes to accelerate the transition towards Net Zero while boosting the competitiveness of EU industry and strengthening domestic supply chains. The Act has been formally adopted by the European Parliament and the Council and will come into force once formally adopted by member states.

US policy

The US policy landscape is made up of national and state legislation, the majority of which is in place to incentivise rather than mandate change. Since rejoining the Paris Agreement in 2021, the US has been ramping up its commitment and action to decarbonise. It is committed to reducing greenhouse gas emissions to 50-52% below 2005 levels by 2030 and achieving Net Zero by 2050.

Inflation Reduction Act (IRA)

The IRA came into force in 2022, designed to curb inflation by spurring investment in green technology and strengthening domestic energy security. It aims to achieve this by providing incentives such as grants and tax credits to both public and private entities that are promoting clean energy.

Through the IRA, a new Alternative Fuel and Low-Emission Aviation Technology competitive grant programme has been launched, alongside two separate tax credits for sustainable fuels. These initiatives aim to close the price-gap between low-carbon and conventional jet fuels, while also providing finance for SAF and hydrogen production scale up. The competitive grant programme also supports aerospace technologies that improve fuel efficiency, increases SAF utilisation, or reduces general aircraft emissions.

Created under the Energy Policy Action (2005), this standard defines the minimum percentage of renewable fuel that must be present in fuel sold each year by importers and suppliers. Although SAF isn’t mandated specifically, credits can be achieved through the provision of SAF if it meets the carbon-saving requirements. The policy is designed to promote biofuels and decarbonise fuel used in transport. However, suppliers can buy-out of obligations, which has meant that the environmental objectives of the standard have largely not been met.

Initially a state-level standard established by California, the Low Carbon Fuel standard has since been adopted by other states, including Washington and Oregon. Fuel suppliers must demonstrate the carbon intensity of transport fuels each year using lifecycle analysis, and demonstrate it meets the carbon intensity standard or acquire credits from other parties for the deficit. It is designed to decrease emissions and increase the range of low-carbon and renewable alternatives, including SAF. In California, a carbon intensity reduction target of 30% has been set for 2030, and new mechanisms have been introduced to adjust targets automatically based on market performance.

International policy

International policy and standards have emerged from the International Civil Aviation Organisation (ICAO) to facilitate cooperation amongst member states and help achieve cohesive global air mobility. This is likely to become increasingly important over the coming decades as new, sustainable fuels and technologies need to be rolled out in a timely way to address the impact of aviation’s greenhouse gas emissions.

The ICAO CO2 emissions standards was adopted to reduce the impact of aviation’s GHG emissions on the climate and it is the world’s first global technology standard for CO2 emissions. This CO2 standard applies to all new aircraft types designs from 2020, and to aircraft type designs already in production that are modified after 2023. By 2028, any aircraft in production that does not meet the standards will not be permitted to be produced. The aim is to encourage more fuel-efficient technologies to be adopted and incorporated into aircraft design.

ICAO noise and air quality standards

Noise and air quality standards also exist for aircraft, including minimum standards that must be met, known as chapters. Over time, these chapters become more stringent helping to mitigate aviation’s environmental impact, particularly for the benefit of communities around airports.

Air quality standards are affected by aviation’s wider, non-CO2 emissions including oxides of nitrogen, carbon monoxide, particulate matter and sulphur compounds.

In March 2024, the ATI published a first-of-its-kind Non-CO2 Technologies Roadmap and announced a funding programme in partnership with Department for Business and Trade and Innovate UK. Find out more here.

Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA)

CORSIA is a global market-based measure to reduce emissions from international aviation with the aim of achieving carbon-neutral growth. Currently in its first phase, the scheme is voluntary until 2027 when participation will become mandatory for all but a handful of small emitting countries. From 2021-2023 participating countries annually reported and offset emissions from aviation that exceeded those emitted during the 2019 baseline year. From 2024 onwards this drops from 100% to 85% of that emitted during the 2019 baseline year. CORSIA is currently anticipated to end in 2035 but by 2032, a special review will be conducted on whether the scheme should be continued after 2035 and if so, what learnings can be applied moving forward.

CORSIA has been criticised by both airlines and NGOs for its shortcomings, as it only aims to achieve carbon-neutral growth rather than applying to all emissions from aviation. The quality of offsets has also been challenged, and ICAO has little power to enforce participation. The details of the scheme have been a compromise to gain support from nations with varying national priorities, and as a result is anticipated to have a reasonably minor impact on the global decarbonisation of aviation compared to other measures.

Further support from the ATI

We hope that this resource has provided a useful overview of the policy landscape, both in the UK and internationally, and has helped you to understand the policy landscape that forms the framework for the industry’s transition to Net Zero. To find out more about the sustainable aviation policy landscape, please follow the links embedded throughout this page or get in touch.

How the ATI Hub can help you

A good place to start is one of our monthly Meet the ATI sessions, where you can talk to us about how the ATI might be able to support your company. To find out more about the wider funding landscape, to give us feedback, or for any questions about the ATI Hub, please get in touch!