Nour Eid • 19.01.23 • 5 min read

Aerospace innovation and the funding landscape

Despite the technology challenge, there is a major economic opportunity for the aerospace sector in achieving Net Zero in aviation by 2050. That was the conclusion of our recently published Funding Growth in Aerospace report which provides a consolidated overview of the funding landscape in aerospace today. The report also highlights opportunities for private investment to capitalise on the growth potential inherent in the Net Zero transformation of the sector.

Unlocking that potential relies on overcoming several hurdles in relation to private financing, including a funding gap for companies within the ‘growth economy’. The report identifies three key challenges for innovators in the UK aerospace sector:

- The UK lags behind the best-in-class in terms of private investment in deep-tech and R&D intensive companies.

- Capital intensive-industries are less attractive to many investors

- Aerospace requires patient capital.

The report analyses the challenges above with data and opinions from a survey of 60 startups and SMEs working in the sector.

A collaboration between the Aerospace Technology Institute (ATI) and PwC, Funding Growth in Aerospace is freely available to read on our website.

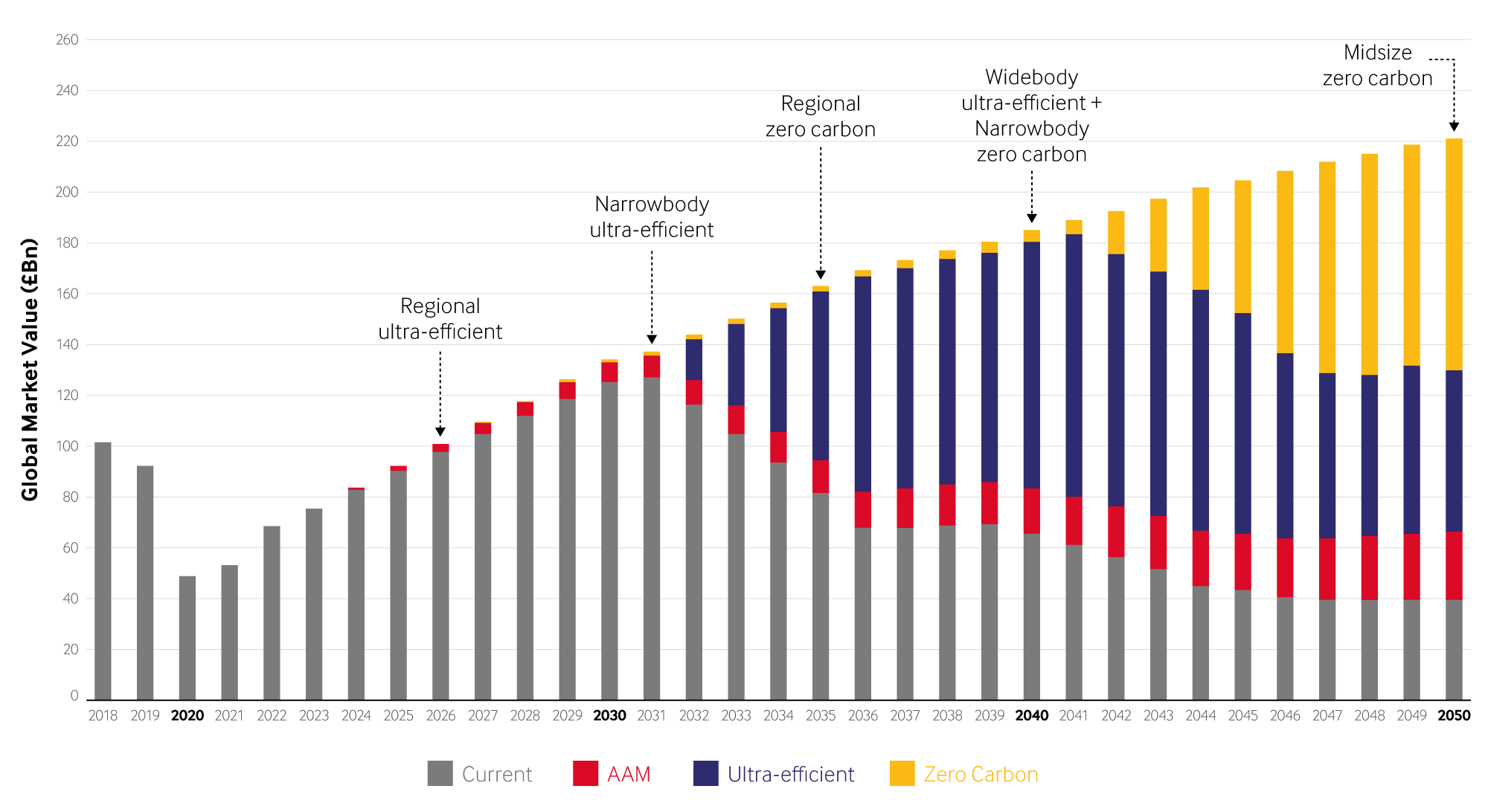

The aerospace sector is preparing for its most significant transformation since the jet age, driven by the need to achieve Net Zero in aviation by 2050. This will require the development of new and in some cases radically different aircraft types, which represent a significant market growth opportunity for UK aerospace companies. The Aerospace Technology Institute (ATI) estimates the global market for new aircraft deliveries at £4.6 trillion from 2022 to 2050.

Opportunities

The ATI’s Market Model Online Tool forecasts a global commercial market of £4.6 trillion from 2022 to 2050 to develop lower emission aircraft. This growth is achieved in three primary segments:

| Aircraft type | Primary technologies | 2050 global annual market | 2050 global market share |

|---|---|---|---|

| Zero-carbon emission | Battery, hydrogen, and fuel cell technologies to enable zero-carbon tailpipe emissions | £91bn | 41% |

| Ultra-efficient aircraft | Ultra-high bypass turbofan engines and a generational light-weighting of aircraft structures and systems. | £64bn | 29% |

| Advanced air mobility | New architectures which enable electric vertical and conventional take-off & landing as well as smaller unmanned aircraft systems. | £27bn | 12% |

The remaining 18% market share from the table above is comprised of the value of this current generation’s aircraft as they are phased out and replaced by ultra-efficient and zero-carbon alternatives.

Market growth

This chart shows the annual growth in the aerospace sector based on deliveries between 2018 and 2050 – the forecasted entry into service of each new aircraft type is highlighted above the chart

{kind=link}

The chart shows the global market for the current fleet of aircraft being superseded by a market for ultra-efficient aircraft from the early 2030s. There is then a further shift towards zero-carbon aircraft from 2040 onwards.

Read more, see the data and join our future events

- Read the full report here: Funding Growth in Aerospace

- The ATI’s Market Model Online Tool allows you to interrogate the data used for the report, and to further analyse market scenarios at more detailed product levels. You can register for free to use the tool here: Market Model Online Tool

- As part of the ATI Hub, we’ll be spending more time focusing on the UK’s aerospace funding landscape. Make sure to keep an eye on our web page to be the first to hear about the clinics we have planned in 2023. Visit the ATI Hub.